Does Home Insurance Cover Your Air Conditioner?

Homeowners insurance generally covers your air conditioner if damage results from specific events like fire, hail, or fallen trees. But it won’t cover normal wear and tear or mechanical breakdowns.

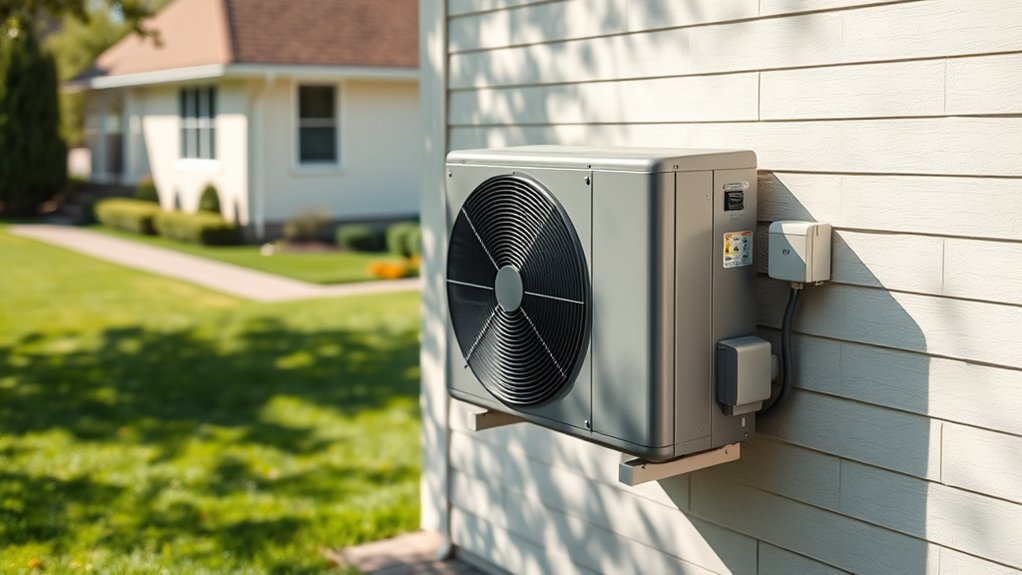

Central AC units fall under dwelling coverage, while window units count as personal property. Each has its own limits and deductibles.

You’ll need to document damage and file claims promptly. Understanding your policy and your maintenance role can really help protect your investment. Explore further for important coverage details.

Homeowners Insurance Coverage for Air Conditioners

Although homeowners insurance can cover your air conditioner if it’s damaged by events like fire, hail, or falling trees, it won’t cover normal wear and tear.

Typically, central air conditioning units are included under dwelling coverage since they’re part of the home’s structure, while window units fall under personal property coverage. Damage caused by covered perils qualifies for claims, but keep in mind that coverage limits and deductibles apply.

Central AC units are covered under dwelling protection; window units fall under personal property coverage with applicable limits.

You can also add equipment breakdown coverage to protect your HVAC system against mechanical failures, but this still excludes general deterioration from everyday use.

To guarantee you’re adequately protected, review your homeowners insurance policy carefully. Understanding your specific coverage will help you know when your air conditioning system is covered and when additional protection might be necessary.

Types of Air Conditioners and Their Insurance Coverage

When it comes to your air conditioner, the coverage really depends on the type you have.

For example, central AC units are usually covered under your dwelling protection.

On the other hand, window units tend to fall under personal property coverage.

Knowing these differences can help you understand exactly what kind of damage is insured—and what isn’t.

Central AC Coverage

Because central air conditioning units are considered part of your home’s structure, your homeowners insurance typically includes them under dwelling coverage. Damage caused by covered perils like hail, lightning, or falling trees is usually covered. But normal wear and tear or mechanical breakdowns aren’t.

An insurance adjuster evaluates claims to determine coverage eligibility. It’s a good idea to review your policy to see if optional endorsements, such as equipment breakdown coverage, apply to your central AC.

| Aspect | Coverage Details |

|---|---|

| Covered Perils | Hail, lightning, falling trees, fire |

| Exclusions | Mechanical breakdown, normal wear and tear |

| Claims Process | Insurance adjuster assesses damage cause |

Understanding these factors guarantees you know how your central air conditioning fits into your homeowners insurance.

Window Unit Protection

Central air conditioning units are covered under your home’s structure, but window AC units fall into a different category. They’re considered personal property in your homeowners insurance.

This means coverage for window AC units depends on your policy specifics and typically applies only to damage caused by covered perils like theft or vandalism.

Normal wear and tear usually isn’t covered. When you file claims for damage, keep in mind that window AC units are subject to personal property coverage limits and deductibles, which vary by insurer.

If an external event, such as a falling tree, damages your window AC unit, it may also be covered.

To guarantee proper protection, review your homeowners insurance policy closely to understand the extent of coverage for your window AC units.

Covered Perils That Qualify HVAC Damage for Insurance Claims

Several common perils can qualify HVAC damage for insurance claims, but you need to understand exactly which events your policy covers. Homeowners insurance typically covers HVAC damage caused by sudden incidents like fire, hailstorms, vandalism, or fallen trees.

However, wear and tear or mechanical failures aren’t included. Central AC units fall under dwelling coverage, while window units count as personal property. When filing claims, verify the damage aligns with your policy’s covered perils and provide necessary documentation for events like vandalism or theft.

| Covered Perils | Coverage Type | Notes |

|---|---|---|

| Fire Incidents | Dwelling | Includes smoke damage |

| Hailstorms | Dwelling | Sudden, accidental damage qualifies |

| Vandalism | Personal Property | Must file proper documentation |

| Fallen Trees | Dwelling | Sudden impact damage covered |

Why Wear and Tear Isn’t Covered by Homeowners Insurance

Although homeowners insurance covers sudden and accidental damage to your air conditioning system, it doesn’t cover wear and tear from regular use and aging. Homeowners insurance policies typically exclude coverage for gradual deterioration. So, claims for normal wear and tear won’t be reimbursed.

This type of insurance focuses on catastrophic events, not the inevitable decline of your air conditioning unit over time. To protect your system, regular maintenance is essential since neglect can lead to issues that aren’t covered.

It’s also important to review your policy’s specific exclusions related to wear and tear.

Unlike homeowners insurance, a home warranty may offer coverage for repairs caused by wear and tear. This can provide an alternative way to manage aging components of your air conditioning unit.

Equipment Breakdown Coverage for HVAC Systems

If you want extra protection for your HVAC system beyond standard homeowners insurance, consider adding Equipment Breakdown Coverage. This optional endorsement covers the repair or replacement of HVAC systems damaged by sudden and accidental events, like electrical surges.

It’s different from typical homeowners insurance because it doesn’t cover general wear and tear or gradual mechanical failures.

Equipment Breakdown Coverage helps fill the gaps left by standard policies that exclude mechanical breakdowns. It’s a smart way to protect yourself from unexpected issues that can get costly.

Equipment Breakdown Coverage bridges the gaps in standard policies, shielding you from costly unexpected HVAC repairs.

Just make sure to review your policy details carefully since coverage limits, deductibles, and specific terms can vary.

By adding this endorsement, you can better safeguard your HVAC system against sudden breakdowns. That way, you won’t be stuck paying for expensive repairs or replacements that your standard homeowners insurance won’t cover.

It’s all about giving you extra peace of mind.

Personal Property Coverage for Window AC Units

Your window AC unit is usually covered under personal property in most homeowners policies.

That means whether it’s protected depends on the specific perils your policy includes.

When you file a claim, remember that limits and deductibles will apply.

Also, if the damage affects the home’s exterior, it might impact your coverage.

Coverage Scope Explained

When you purchase homeowners insurance, window air conditioning units fall under personal property coverage rather than the structure of your home. This means your AC unit is treated as a personal belonging, so damage or theft caused by covered perils like fire or vandalism is typically covered.

However, repair or replacement costs depend on the personal property limits and deductibles outlined in your policy.

It’s important to review your insurance policy carefully since coverage details for window AC units can vary between providers.

Keep in mind that normal wear and tear or mechanical breakdowns usually aren’t covered, leaving those repairs your responsibility.

Understanding these distinctions helps you manage expectations and protect your investment effectively.

Claim Process Overview

Filing a claim for a window air conditioning unit involves several key steps to confirm your personal property coverage applies correctly.

First, review your policy to understand what homeowners insurance covers HVAC units like yours and note any specific limits or exclusions.

Next, document the damaged HVAC thoroughly with photos and detailed descriptions.

Then, contact your insurer promptly to file a claim, providing all necessary evidence of the damage.

Keep in mind, insurance claims for window AC units often exclude damage due to wear and tear or neglect.

The claim process overview typically involves an adjuster’s assessment to verify the cause and extent of damage.

Knowing how your policy covers your window AC helps you navigate claims efficiently and avoid surprises during settlement.

It’s always a good idea to be prepared and informed so the whole process goes smoothly.

Policy Limitations Noted

Understanding the claim process is important, but it’s just as important to recognize the limitations your policy places on coverage for window air conditioning units.

In homeowners insurance, window AC units fall under personal property. This is separate from central HVAC systems, which are covered under dwelling protection.

Coverage usually applies only to damage caused by specific perils like fire or theft. It doesn’t cover wear and tear or mechanical failure. Claims for your AC unit are subject to personal property coverage limits and deductibles, which can vary depending on your policy.

If damage happens from an external event affecting the home, coverage might apply. But you’ll need to check your policy details carefully to be sure.

Being aware of these coverage limits helps you manage expectations and get ready for any possible out-of-pocket costs when filing a claim.

Filing an HVAC Insurance Claim: What to Expect

Although submitting an HVAC insurance claim can feel overwhelming, knowing what to expect helps you navigate the process smoothly.

First, your insurer may send an adjuster to assess the damage and verify if it qualifies under your coverage.

You should document the damage thoroughly with photos and videos, as the insurance provider often requests this evidence.

If your claim is approved, it may cover repair or replacement costs, but keep in mind your deductible will apply. Filing a claim makes financial sense only if repair costs exceed this deductible.

Also, be aware reimbursement depends on your policy type. Some provide replacement value, while others pay actual cash value for the damaged unit.

Understanding these steps guarantees you handle your HVAC insurance claim effectively.

HVAC Maintenance Tips to Avoid Homeowners Insurance Claim Denials

Once you know what to expect when filing an HVAC insurance claim, the best way to protect yourself is by maintaining your system properly. Regular HVAC maintenance, like changing or cleaning air filters every 1-3 months and scheduling professional check-ups annually, helps prevent system breaks that lead to costly repairs.

Proper HVAC maintenance, including regular filter changes and annual check-ups, prevents costly repairs and protects your insurance claim.

Keeping outdoor units free from debris and following manufacturer installation guidelines also reduces risks. Since homeowners insurance covers AC damage only under certain conditions, you should document all maintenance and repairs with receipts and service records. This proof shows you’ve taken proper care, increasing the chance your insurance may cover HVAC issues.

Remember, your policy won’t cover damage caused by neglect or improper use, so staying proactive is key to avoiding claim denials when it’s time to repair or replace components.

It’s really all about staying on top of things and keeping good records. That way, you’re in a much better position if you ever need to file a claim.

Comparing HVAC Warranties and Homeowners Insurance Coverage

When you compare HVAC warranties and homeowners insurance coverage, it becomes clear that each serves a different purpose in protecting your air conditioning system.

Homeowners insurance typically covers damage from specific perils like fire or hail under dwelling coverage but excludes normal wear and tear or mechanical failures.

In contrast, HVAC warranties focus on repairs or replacements caused by mechanical failures and wear and tear, which insurance usually doesn’t address.

Window AC units fall under personal property, so their coverage differs from central systems. You can also add equipment breakdown coverage to your homeowners insurance to protect against mechanical issues.

Understanding these differences helps you safeguard your air conditioning system effectively.

This way, you’re covered for sudden damage through insurance and for ongoing maintenance via HVAC warranties.

Getting a Homeowners Insurance Quote for HVAC Coverage

You can quickly get homeowners insurance quotes online that are tailored to your HVAC system type.

These tools provide instant rate estimates and personalized coverage options based on what you need.

Just be sure to review the details carefully to make sure your air conditioner is properly protected.

Easy Online Quotes

Many homeowners find that obtaining a homeowners insurance quote for HVAC coverage takes just a few clicks online. This quick access to online quotes lets you check out coverage options from different insurance providers easily.

Since a standard homeowners insurance policy mightn’t always cover your AC unit fully, it’s a good idea to review the details carefully.

If your HVAC system gets damaged, your insurance policy may cover repairs or replacement depending on the cause and coverage limits. Using online tools, you can compare rates and see how well each policy protects you against potential HVAC damage.

This way, you can make smarter decisions about what coverage you really need. Plus, understanding your protection helps you feel more confident about what’s covered if your HVAC system runs into trouble.

It’s all about finding the right fit for your home and budget without any hassle.

Personalized Coverage Options

Although standard homeowners insurance provides general protection, obtaining a personalized quote helps you understand how your HVAC system, whether a central AC or window unit, is specifically covered.

A home insurance policy often treats central AC units as part of the dwelling, offering protection against perils like fire or storms.

In contrast, window AC units usually fall under personal property coverage, with distinct coverage limits and deductibles.

When you request a quote, you can also explore optional equipment breakdown coverage to protect HVAC systems from mechanical failures and electrical surges.

Reviewing your quote lets you identify exclusions related to normal wear and tear, which typically aren’t covered.

Getting a detailed quote guarantees your policy matches your needs and provides clear insights into HVAC coverage options.

Instant Rate Estimates

Understanding how your HVAC system fits into your homeowners insurance coverage is just the start. Getting instant rate estimates helps you grasp the potential costs of protecting your air conditioning units.

Here’s how to efficiently get a homeowners insurance quote for HVAC coverage: Use online tools to enter specific details about your HVAC systems for tailored quotes.

Then, compare quotes from multiple insurers to spot differences in coverage options and premiums.

Next, review coverage limits and deductibles related to HVAC protection in each quote. Also, consider additional endorsements like equipment breakdown coverage for thorough HVAC safeguard.

These steps guarantee you make informed decisions about your policy, balancing cost with adequate protection for your home’s cooling systems.

It’s all about finding the best fit for your needs.

Frequently Asked Questions

Can Flood Insurance Cover Air Conditioner Damage?

Flood insurance can cover air conditioner damage, but it really depends on your policy’s coverage limits and exclusions.

You’ll need to take a close look at your flood insurance since many policies exclude direct water damage to AC units.

To make the insurance claims process easier, it helps to keep records of AC maintenance and replacement costs.

Knowing about policy exclusions ahead of time can save you from surprises when it comes to out-of-pocket expenses related to flood or water damage to your air conditioner.

Does Renters Insurance Cover Window AC Units?

Think of renters insurance coverage like a safety net catching your window AC unit if it’s stolen or damaged by fire. It generally covers window air conditioner types as personal property, subject to coverage limits and deductible amounts.

However, policy exclusions often exclude wear and tear or mechanical failure. Replacement value and installation costs mightn’t be fully covered, so review your policy carefully before filing a claim.

This way, you understand the claims process and limits. It’s always good to be clear on what’s included and what’s not.

How Does Insurance Handle AC Replacement After a Total Loss?

When handling AC replacement after a total loss, your insurer will assess the replacement costs based on your policy details. This includes coverage limits and the replacement value.

They also take into account your air conditioner’s age and maintenance records during the claim process.

It really helps to document everything carefully. Total loss claims usually need an adjuster to evaluate and confirm if you’re eligible.

Knowing your insurance policy details upfront makes a big difference. That way, you’ll understand whether you get actual cash value or full replacement reimbursement.

Are Portable Air Conditioners Covered Under Home Insurance?

Think of your portable air conditioner as a small ship in a vast insurance ocean. Your coverage depends on the policy limits.

Portable unit coverage usually protects against theft or damage from covered perils, but not equipment breakdown or wear.

Keep your maintenance records handy for claims. Remember, deductible considerations and seasonal use can impact your payout.

Also, check if your home warranty overlaps with your insurance to avoid gaps or duplicates in protection.

Will Insurance Cover AC Damage From Power Surges?

Insurance typically won’t cover AC damage from power surges unless you have specific endorsements like Equipment Breakdown Coverage.

You should review the coverage exclusions explained in your policy and understand the insurance claim process.

Investing in power surge protection through surge protector installation and electrical system upgrades can really help prevent damage.

Regular air conditioner maintenance and checking appliance replacement values also protect your investment.

You might want to consider home warranty plans for added coverage beyond standard insurance.

They can offer extra peace of mind when it comes to your appliances.

Conclusion

When considering coverage for your air conditioner, understanding homeowners insurance is essential. While sudden storms and accidents might spark a claim, standard policies seldom cover steady wear and tear. Protect your prized HVAC with regular maintenance and consider equipment breakdown coverage for added security.

By balancing warranties with insurance, you’ll breeze through potential breakdowns smoothly. Stay savvy, stay secure, and guarantee your cool comfort is consistently covered.